Home

Home

Back

Back

Definition: This calculator computes the Final Balance (\( B_{\text{final}} \)) and Interest Earned (\( I \)) for an investment or savings account based on the Initial Balance (\( B_0 \)), Interest Rate (\( r \)), Term (\( t \)), Compounding Frequency (\( n \)), and optional Periodic Deposit (\( D \)).

Purpose: Savers and investors use this tool to estimate the growth of their money over time, helping to plan for future financial goals or compare investment options.

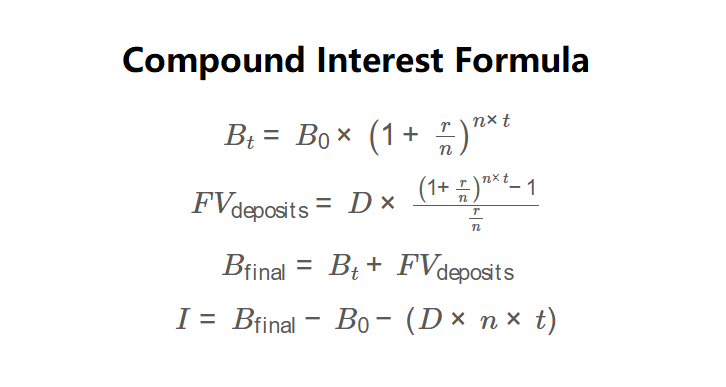

The calculator uses the following formulas, as shown in the image above:

\( B_t = B_0 \times \left(1 + \frac{r}{n}\right)^{n \times t} \)

\( FV_{\text{deposits}} = D \times \frac{\left(1 + \frac{r}{n}\right)^{n \times t} - 1}{\frac{r}{n}} \)

\( B_{\text{final}} = B_t + FV_{\text{deposits}} \)

\( I = B_{\text{final}} - B_0 - (D \times n \times t) \)

Where:

Steps:

Calculating compound interest is essential for:

Q: Why does compounding frequency matter?

A: More frequent compounding increases the effective interest rate, leading to higher returns over the same term.

Q: Can the interest rate be negative?

A: While rare, negative interest rates can occur in certain economic conditions. The calculator allows this, but it’s not typical for savings accounts.

Q: What if I don’t make periodic deposits?

A: If no periodic deposits are made (\( D = 0 \)), the calculator computes the growth based solely on the Initial Balance and interest rate.